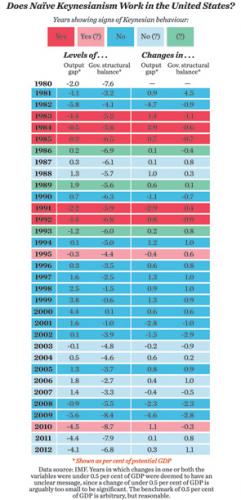

In my book Money in a Free Society (Encounter Books), there is a chapter on Friedman's critique of fiscal policy, which included a box with the IMF data for changes in the US structural budget balance and the output gap going back to 1981. I found clear evidence in support of Keynesianism in only five years, less than a fifth of the period of 28 years from 1981 to 2008 inclusive. There were twice as many years in which the structural budget balance and the output gap moved in the same direction, which contradicted Keynesian thinking.

We now have four more years of data, and the 2012 outcome is more or less known. Some revisions have also been made to the data for the 1981-2008 period, although these are minor. The accompanying box (right) gives the numbers for the 32 years from 1981 to 2012 inclusive. Does the addition of the Great Recession period help the Keynesians? The answer is, no, quite the reverse. In the 32 years we still have five years (1983, 1984, 1985, 1991 and 1992) in which the structural budget balance and the output gap changed in opposite directions by significant amounts, in line with the Keynesian view. But we now have no fewer than 14 years in which the structural budget balance and the output gap clearly moved in the same direction. We might call these the anti-Keynesian years, while the balance of 13 years that have an unclear pattern or insignificant numbers of under 0.5 per cent of GDP might be called non-Keynesian. In the last three decades the anti-Keynesian and non-Keynesian years have outnumbered the Keynesian years by more than six to one.

My message is both basic for the debate on the fiscal cliff and totally at variance with the fundamental premise that underlies it. The historical record shows that since 1980 there have been almost three times as many years in which policy action to reduce the budget deficit has been associated with above-trend growth, or increasing the deficit has come with beneath-trend growth or falling output than not. More succinctly, the data imply that—if Obama and Congress fail to agree on anything—the plunge in the budgetdeficit will be positive for demand, jobs and employment in 2013. The fiscal cliff is good for economic expansion, not bad. So not only Keynesians like Joseph Stiglitz, but the entire circus of international macroeconomic pundits have been talking rot.

- Mr Cameron, Show The Country That You Care

- Campaign Diary

- Defying Duopoly: The Rise Of The Insurgents

- Don't Rig The System In Favour Of Coalitions

- Warring Gangsters Who Run The Country

- Political Correctness Is Devouring Itself

- An Archival Treasure Trove—And All Online

- Do we value freedom of speech in Britain?

- Can Europe's Jews Feel Safe Alongside Muslims?

- We Cannot Avoid The Battle Over Blasphemy

- Inside The World Of 'Non-Violent' Islamism

- We Can Fix The Economy But Not Human Nature

- The Keynesian Versus The Monetarist: A Lost Decade

- The Keynesian Versus The Monetarist: Time To Re-Read Keynes

- The New Language Of Political Narcissism

- Two Words You Won't Hear This Election: Foreign Policy

- The Many Faces Of Holocaust Denial

- Why Is 'Fifty Shades of Grey' the New Normal?

- Obama scuttles. America retreats. Things fall apart

- Putin and the Art of Political Fantasy

9:02 AM